0001616262

Rocky Mountain Chocolate Factory, Inc.

false

--02-28

FY

2023

646,394

620,798

625,526

666,315

804,815

35,173

47,228

38,778

65,059

0.001

0.001

250,000

250,000

0

0

0

0

0.001

0.001

46,000,000

46,000,000

6,257,137

6,257,137

6,186,356

6,186,356

2

5

39

5

6

1

1

1

1

1

1

10

3

5

10

5

20

10

5

10

70,000

6

18

5

6

0

488,695

0.08

0.03

0.08

0.03

70,000

00016162622022-03-012023-02-28

iso4217:USD

00016162622022-08-31

xbrli:shares

00016162622023-05-19

thunderdome:item

0001616262us-gaap:ProductMember2022-03-012023-02-28

0001616262us-gaap:ProductMember2021-03-012022-02-28

0001616262us-gaap:ProductMember2020-03-012021-02-28

0001616262rmcf:FranchiseAndRoyaltyFeesMember2022-03-012023-02-28

0001616262rmcf:FranchiseAndRoyaltyFeesMember2021-03-012022-02-28

0001616262rmcf:FranchiseAndRoyaltyFeesMember2020-03-012021-02-28

00016162622021-03-012022-02-28

00016162622020-03-012021-02-28

0001616262us-gaap:FranchiseMember2022-03-012023-02-28

0001616262us-gaap:FranchiseMember2021-03-012022-02-28

0001616262us-gaap:FranchiseMember2020-03-012021-02-28

0001616262us-gaap:RetailMember2022-03-012023-02-28

0001616262us-gaap:RetailMember2021-03-012022-02-28

0001616262us-gaap:RetailMember2020-03-012021-02-28

iso4217:USDxbrli:shares

00016162622023-02-28

00016162622022-02-28

0001616262us-gaap:CommonStockMember2022-02-28

0001616262us-gaap:CommonStockMember2021-02-28

0001616262us-gaap:CommonStockMember2020-02-29

0001616262us-gaap:CommonStockMember2022-03-012023-02-28

0001616262us-gaap:CommonStockMember2021-03-012022-02-28

0001616262us-gaap:CommonStockMember2020-03-012021-02-28

0001616262us-gaap:CommonStockMember2023-02-28

0001616262us-gaap:AdditionalPaidInCapitalMember2022-02-28

0001616262us-gaap:AdditionalPaidInCapitalMember2021-02-28

0001616262us-gaap:AdditionalPaidInCapitalMember2020-02-29

0001616262us-gaap:AdditionalPaidInCapitalMember2022-03-012023-02-28

0001616262us-gaap:AdditionalPaidInCapitalMember2021-03-012022-02-28

0001616262us-gaap:AdditionalPaidInCapitalMember2020-03-012021-02-28

0001616262us-gaap:AdditionalPaidInCapitalMember2023-02-28

0001616262us-gaap:RetainedEarningsMember2022-02-28

0001616262us-gaap:RetainedEarningsMember2021-02-28

0001616262us-gaap:RetainedEarningsMember2020-02-29

0001616262us-gaap:RetainedEarningsMember2022-03-012023-02-28

0001616262us-gaap:RetainedEarningsMember2021-03-012022-02-28

0001616262us-gaap:RetainedEarningsMember2020-03-012021-02-28

0001616262us-gaap:RetainedEarningsMember2023-02-28

00016162622021-02-28

00016162622020-02-29

0001616262rmcf:EdibleMember2022-03-012023-02-28

0001616262rmcf:EdibleMember2021-03-012022-02-28

0001616262rmcf:EdibleMember2020-03-012021-02-28

xbrli:pure

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:CompanyOwnedStoresMemberrmcf:StoresOpenedAt2282022Member2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:CompanyOwnedStoresMemberrmcf:OpenMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:CompanyOwnedStoresMemberrmcf:ClosedMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:CompanyOwnedStoresMemberrmcf:SoldMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:CompanyOwnedStoresMemberrmcf:StoresOpenedAt22823Member2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:CompanyOwnedStoresMemberrmcf:SoldNotYetOpenMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:CompanyOwnedStoresMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:FranchiseStoresDomesticStoresAndKiosksMemberrmcf:StoresOpenedAt2282022Member2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:FranchiseStoresDomesticStoresAndKiosksMemberrmcf:OpenMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:FranchiseStoresDomesticStoresAndKiosksMemberrmcf:ClosedMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:FranchiseStoresDomesticStoresAndKiosksMemberrmcf:SoldMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:FranchiseStoresDomesticStoresAndKiosksMemberrmcf:StoresOpenedAt22823Member2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:FranchiseStoresDomesticStoresAndKiosksMemberrmcf:SoldNotYetOpenMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:FranchiseStoresDomesticStoresAndKiosksMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:InternationalLicenseStoresMemberrmcf:StoresOpenedAt2282022Member2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:InternationalLicenseStoresMemberrmcf:OpenMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:InternationalLicenseStoresMemberrmcf:ClosedMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:InternationalLicenseStoresMemberrmcf:SoldMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:InternationalLicenseStoresMemberrmcf:StoresOpenedAt22823Member2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:InternationalLicenseStoresMemberrmcf:SoldNotYetOpenMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:InternationalLicenseStoresMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:ColdStoneCreameryCobrandedMemberrmcf:StoresOpenedAt2282022Member2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:ColdStoneCreameryCobrandedMemberrmcf:OpenMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:ColdStoneCreameryCobrandedMemberrmcf:ClosedMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:ColdStoneCreameryCobrandedMemberrmcf:SoldMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:ColdStoneCreameryCobrandedMemberrmcf:StoresOpenedAt22823Member2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:ColdStoneCreameryCobrandedMemberrmcf:SoldNotYetOpenMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:ColdStoneCreameryCobrandedMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:USwirlIncMemberrmcf:StoresOpenedAt2282022Member2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:USwirlIncMemberrmcf:OpenMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:USwirlIncMemberrmcf:ClosedMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:USwirlIncMemberrmcf:SoldMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:USwirlIncMemberrmcf:StoresOpenedAt22823Member2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:USwirlIncMemberrmcf:SoldNotYetOpenMember2023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMemberrmcf:USwirlIncMember2023-02-28

0001616262rmcf:StoresOpenedAt2282022Member2023-02-28

0001616262rmcf:OpenMember2023-02-28

0001616262rmcf:ClosedMember2023-02-28

0001616262rmcf:SoldMember2023-02-28

0001616262rmcf:StoresOpenedAt22823Member2023-02-28

0001616262rmcf:SoldNotYetOpenMember2023-02-28

0001616262srt:MinimumMember2023-02-28

0001616262srt:MaximumMember2023-02-28

utr:Y

0001616262srt:MinimumMember2022-03-28

0001616262srt:MaximumMember2022-03-28

0001616262us-gaap:FranchiseRightsMembersrt:MinimumMember2023-02-28

0001616262srt:MinimumMember2021-03-012022-02-28

0001616262srt:MaximumMember2021-03-012022-02-28

0001616262us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedPaymentArrangementNonemployeeMember2022-03-012023-02-28

0001616262us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedPaymentArrangementNonemployeeMember2021-03-012022-02-28

0001616262us-gaap:RestrictedStockMembersrt:MinimumMemberrmcf:AnnualVestingMember2022-03-012023-02-28

0001616262us-gaap:RestrictedStockUnitsRSUMembersrt:MaximumMemberrmcf:AnnualVestingMember2021-03-012022-02-28

0001616262us-gaap:RestrictedStockUnitsRSUMemberrmcf:AnnualVestingMember2021-03-012022-02-28

0001616262us-gaap:RestrictedStockUnitsRSUMembersrt:MinimumMember2021-03-012022-02-28

0001616262us-gaap:RestrictedStockUnitsRSUMembersrt:MaximumMember2021-03-012022-02-28

0001616262us-gaap:RestrictedStockUnitsRSUMember2022-03-012023-02-28

0001616262us-gaap:RestrictedStockUnitsRSUMember2021-03-012022-02-28

0001616262us-gaap:RestrictedStockUnitsRSUMember2021-02-28

0001616262us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedPaymentArrangementEmployeeMember2023-02-28

0001616262us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedPaymentArrangementEmployeeMember2022-03-012023-02-28

0001616262us-gaap:ShareBasedPaymentArrangementNonemployeeMember2021-03-012022-02-28

0001616262us-gaap:ShareBasedPaymentArrangementNonemployeeMember2022-03-012023-02-28

0001616262us-gaap:ShareBasedPaymentArrangementNonemployeeMember2020-03-012021-02-28

0001616262srt:ChiefExecutiveOfficerMember2022-03-012023-02-28

0001616262us-gaap:PerformanceSharesMembersrt:MaximumMembersrt:ChiefExecutiveOfficerMember2022-03-012023-02-28

0001616262us-gaap:PerformanceSharesMembersrt:ChiefExecutiveOfficerMember2022-03-012023-02-28

0001616262us-gaap:PerformanceSharesMembersrt:ChiefExecutiveOfficerMemberrmcf:VestingOnLastDayOfCurrentFiscalYearEndingMember2022-03-012023-02-28

0001616262us-gaap:PerformanceSharesMembersrt:MinimumMembersrt:ChiefExecutiveOfficerMember2022-03-012023-02-28

0001616262us-gaap:WarrantMember2022-03-012023-02-28

0001616262rmcf:UnvestedRestrictedStockUnitsMember2022-03-012023-02-28

0001616262us-gaap:WarrantMember2021-03-012022-02-28

0001616262rmcf:UnvestedRestrictedStockUnitsMember2021-03-012022-02-28

0001616262us-gaap:WarrantMember2020-03-012021-02-28

0001616262rmcf:UnvestedRestrictedStockUnitsMember2020-03-012021-02-28

0001616262rmcf:RockyMountainChocolateFactoryMember2022-03-012023-02-28

0001616262rmcf:RockyMountainChocolateFactoryMember2021-03-012022-02-28

0001616262rmcf:RockyMountainChocolateFactoryMember2020-03-012021-02-28

0001616262rmcf:USwirlIncMemberus-gaap:SubsequentEventMember2023-05-01

0001616262rmcf:USwirlIncMemberus-gaap:SubsequentEventMember2023-05-012023-05-01

0001616262us-gaap:SubsequentEventMember2023-05-082023-05-08

0001616262us-gaap:RestrictedStockUnitsRSUMemberus-gaap:SubsequentEventMember2023-05-082023-05-08

0001616262srt:MaximumMemberus-gaap:SubsequentEventMember2023-05-082023-05-08

0001616262srt:MaximumMember2022-03-012023-02-28

0001616262srt:MinimumMember2022-03-012023-02-28

00016162622024-03-012023-02-28

00016162622025-03-012023-02-28

00016162622026-03-012023-02-28

00016162622027-03-012023-02-28

00016162622028-03-012023-02-28

00016162622029-03-012023-02-28

0001616262rmcf:FranchiseFeesMemberrmcf:FranchisingMemberus-gaap:TransferredOverTimeMember2022-03-012023-02-28

0001616262rmcf:FranchiseFeesMemberrmcf:ManufacturingMemberus-gaap:TransferredOverTimeMember2022-03-012023-02-28

0001616262rmcf:FranchiseFeesMemberrmcf:RetailSegmentMemberus-gaap:TransferredOverTimeMember2022-03-012023-02-28

0001616262rmcf:FranchiseFeesMemberrmcf:USwirlIncMemberus-gaap:TransferredOverTimeMember2022-03-012023-02-28

0001616262rmcf:FactorySalesMemberrmcf:FranchisingMemberus-gaap:TransferredAtPointInTimeMember2022-03-012023-02-28

0001616262rmcf:FactorySalesMemberrmcf:ManufacturingMemberus-gaap:TransferredAtPointInTimeMember2022-03-012023-02-28

0001616262rmcf:FactorySalesMemberrmcf:RetailSegmentMemberus-gaap:TransferredAtPointInTimeMember2022-03-012023-02-28

0001616262rmcf:FactorySalesMemberrmcf:USwirlIncMemberus-gaap:TransferredAtPointInTimeMember2022-03-012023-02-28

0001616262us-gaap:RetailMemberrmcf:FranchisingMemberus-gaap:TransferredAtPointInTimeMember2022-03-012023-02-28

0001616262us-gaap:RetailMemberrmcf:ManufacturingMemberus-gaap:TransferredAtPointInTimeMember2022-03-012023-02-28

0001616262us-gaap:RetailMemberrmcf:RetailSegmentMemberus-gaap:TransferredAtPointInTimeMember2022-03-012023-02-28

0001616262us-gaap:RetailMemberrmcf:USwirlIncMemberus-gaap:TransferredAtPointInTimeMember2022-03-012023-02-28

0001616262rmcf:RoyaltyAndMarketingFeesMemberrmcf:FranchisingMemberus-gaap:TransferredAtPointInTimeMember2022-03-012023-02-28

0001616262rmcf:RoyaltyAndMarketingFeesMemberrmcf:ManufacturingMemberus-gaap:TransferredAtPointInTimeMember2022-03-012023-02-28

0001616262rmcf:RoyaltyAndMarketingFeesMemberrmcf:RetailSegmentMemberus-gaap:TransferredAtPointInTimeMember2022-03-012023-02-28

0001616262rmcf:RoyaltyAndMarketingFeesMemberrmcf:USwirlIncMemberus-gaap:TransferredAtPointInTimeMember2022-03-012023-02-28

0001616262rmcf:FranchisingMemberus-gaap:TransferredAtPointInTimeMember2022-03-012023-02-28

0001616262rmcf:ManufacturingMemberus-gaap:TransferredAtPointInTimeMember2022-03-012023-02-28

0001616262rmcf:RetailSegmentMemberus-gaap:TransferredAtPointInTimeMember2022-03-012023-02-28

0001616262rmcf:USwirlIncMemberus-gaap:TransferredAtPointInTimeMember2022-03-012023-02-28

0001616262rmcf:FranchiseFeesMemberrmcf:FranchisingMemberus-gaap:TransferredOverTimeMember2021-03-012022-02-28

0001616262rmcf:FranchiseFeesMemberrmcf:ManufacturingMemberus-gaap:TransferredOverTimeMember2021-03-012022-02-28

0001616262rmcf:FranchiseFeesMemberrmcf:RetailSegmentMemberus-gaap:TransferredOverTimeMember2021-03-012022-02-28

0001616262rmcf:FranchiseFeesMemberrmcf:USwirlIncMemberus-gaap:TransferredOverTimeMember2021-03-012022-02-28

0001616262rmcf:FactorySalesMemberrmcf:FranchisingMemberus-gaap:TransferredAtPointInTimeMember2021-03-012022-02-28

0001616262rmcf:FactorySalesMemberrmcf:ManufacturingMemberus-gaap:TransferredAtPointInTimeMember2021-03-012022-02-28

0001616262rmcf:FactorySalesMemberrmcf:RetailSegmentMemberus-gaap:TransferredAtPointInTimeMember2021-03-012022-02-28

0001616262rmcf:FactorySalesMemberrmcf:USwirlIncMemberus-gaap:TransferredAtPointInTimeMember2021-03-012022-02-28

0001616262us-gaap:RetailMemberrmcf:FranchisingMemberus-gaap:TransferredAtPointInTimeMember2021-03-012022-02-28

0001616262us-gaap:RetailMemberrmcf:ManufacturingMemberus-gaap:TransferredAtPointInTimeMember2021-03-012022-02-28

0001616262us-gaap:RetailMemberrmcf:RetailSegmentMemberus-gaap:TransferredAtPointInTimeMember2021-03-012022-02-28

0001616262us-gaap:RetailMemberrmcf:USwirlIncMemberus-gaap:TransferredAtPointInTimeMember2021-03-012022-02-28

0001616262rmcf:RoyaltyAndMarketingFeesMemberrmcf:FranchisingMemberus-gaap:TransferredAtPointInTimeMember2021-03-012022-02-28

0001616262rmcf:RoyaltyAndMarketingFeesMemberrmcf:ManufacturingMemberus-gaap:TransferredAtPointInTimeMember2021-03-012022-02-28

0001616262rmcf:RoyaltyAndMarketingFeesMemberrmcf:RetailSegmentMemberus-gaap:TransferredAtPointInTimeMember2021-03-012022-02-28

0001616262rmcf:RoyaltyAndMarketingFeesMemberrmcf:USwirlIncMemberus-gaap:TransferredAtPointInTimeMember2021-03-012022-02-28

0001616262rmcf:FranchisingMemberus-gaap:TransferredAtPointInTimeMember2021-03-012022-02-28

0001616262rmcf:ManufacturingMemberus-gaap:TransferredAtPointInTimeMember2021-03-012022-02-28

0001616262rmcf:RetailSegmentMemberus-gaap:TransferredAtPointInTimeMember2021-03-012022-02-28

0001616262rmcf:USwirlIncMemberus-gaap:TransferredAtPointInTimeMember2021-03-012022-02-28

0001616262rmcf:FranchiseFeesMemberrmcf:FranchisingMemberus-gaap:TransferredOverTimeMember2020-03-012021-02-28

0001616262rmcf:FranchiseFeesMemberrmcf:ManufacturingMemberus-gaap:TransferredOverTimeMember2020-03-012021-02-28

0001616262rmcf:FranchiseFeesMemberrmcf:RetailSegmentMemberus-gaap:TransferredOverTimeMember2020-03-012021-02-28

0001616262rmcf:FranchiseFeesMemberrmcf:USwirlIncMemberus-gaap:TransferredOverTimeMember2020-03-012021-02-28

0001616262rmcf:FactorySalesMemberrmcf:FranchisingMemberus-gaap:TransferredAtPointInTimeMember2020-03-012021-02-28

0001616262rmcf:FactorySalesMemberrmcf:ManufacturingMemberus-gaap:TransferredAtPointInTimeMember2020-03-012021-02-28

0001616262rmcf:FactorySalesMemberrmcf:RetailSegmentMemberus-gaap:TransferredAtPointInTimeMember2020-03-012021-02-28

0001616262rmcf:FactorySalesMemberrmcf:USwirlIncMemberus-gaap:TransferredAtPointInTimeMember2020-03-012021-02-28

0001616262us-gaap:RetailMemberrmcf:FranchisingMemberus-gaap:TransferredAtPointInTimeMember2020-03-012021-02-28

0001616262us-gaap:RetailMemberrmcf:ManufacturingMemberus-gaap:TransferredAtPointInTimeMember2020-03-012021-02-28

0001616262us-gaap:RetailMemberrmcf:RetailSegmentMemberus-gaap:TransferredAtPointInTimeMember2020-03-012021-02-28

0001616262us-gaap:RetailMemberrmcf:USwirlIncMemberus-gaap:TransferredAtPointInTimeMember2020-03-012021-02-28

0001616262rmcf:RoyaltyAndMarketingFeesMemberrmcf:FranchisingMemberus-gaap:TransferredAtPointInTimeMember2020-03-012021-02-28

0001616262rmcf:RoyaltyAndMarketingFeesMemberrmcf:ManufacturingMemberus-gaap:TransferredAtPointInTimeMember2020-03-012021-02-28

0001616262rmcf:RoyaltyAndMarketingFeesMemberrmcf:RetailSegmentMemberus-gaap:TransferredAtPointInTimeMember2020-03-012021-02-28

0001616262rmcf:RoyaltyAndMarketingFeesMemberrmcf:USwirlIncMemberus-gaap:TransferredAtPointInTimeMember2020-03-012021-02-28

0001616262rmcf:FranchisingMemberus-gaap:TransferredAtPointInTimeMember2020-03-012021-02-28

0001616262rmcf:ManufacturingMemberus-gaap:TransferredAtPointInTimeMember2020-03-012021-02-28

0001616262rmcf:RetailSegmentMemberus-gaap:TransferredAtPointInTimeMember2020-03-012021-02-28

0001616262rmcf:USwirlIncMemberus-gaap:TransferredAtPointInTimeMember2020-03-012021-02-28

0001616262us-gaap:LandMember2023-02-28

0001616262us-gaap:LandMember2022-02-28

0001616262us-gaap:BuildingMember2023-02-28

0001616262us-gaap:BuildingMember2022-02-28

0001616262us-gaap:MachineryAndEquipmentMember2023-02-28

0001616262us-gaap:MachineryAndEquipmentMember2022-02-28

0001616262us-gaap:FurnitureAndFixturesMember2023-02-28

0001616262us-gaap:FurnitureAndFixturesMember2022-02-28

0001616262us-gaap:LeaseholdImprovementsMember2023-02-28

0001616262us-gaap:LeaseholdImprovementsMember2022-02-28

0001616262us-gaap:TransportationEquipmentMember2023-02-28

0001616262us-gaap:TransportationEquipmentMember2022-02-28

0001616262rmcf:StoreDesignMember2023-02-28

0001616262rmcf:StoreDesignMember2022-02-28

0001616262rmcf:PackagingLicensesMembersrt:MinimumMember2023-02-28

0001616262rmcf:PackagingLicensesMembersrt:MaximumMember2023-02-28

0001616262rmcf:PackagingLicensesMember2023-02-28

0001616262rmcf:PackagingLicensesMember2022-02-28

0001616262rmcf:PackagingDesignMember2023-02-28

0001616262rmcf:PackagingDesignMember2022-02-28

0001616262rmcf:TrademarksAndNonCompetitionAgreementMembersrt:MinimumMember2023-02-28

0001616262rmcf:TrademarksAndNonCompetitionAgreementMembersrt:MaximumMember2023-02-28

0001616262rmcf:TrademarksAndNonCompetitionAgreementMember2023-02-28

0001616262rmcf:TrademarksAndNonCompetitionAgreementMember2022-02-28

0001616262rmcf:CompanyStoresGoodwillMember2023-02-28

0001616262rmcf:CompanyStoresGoodwillMember2022-02-28

0001616262rmcf:FranchisingGoodwillMember2023-02-28

0001616262rmcf:FranchisingGoodwillMember2022-02-28

0001616262rmcf:ManufacturingSegmentGoodwillMember2023-02-28

0001616262rmcf:ManufacturingSegmentGoodwillMember2022-02-28

0001616262us-gaap:TrademarksMember2023-02-28

0001616262us-gaap:TrademarksMember2022-02-28

0001616262rmcf:CompanyStoresGoodwillMember2022-03-012023-02-28

0001616262us-gaap:GeneralAndAdministrativeExpenseMemberrmcf:Covid19PandemicMember2020-03-012020-05-31

0001616262us-gaap:GeneralAndAdministrativeExpenseMemberrmcf:Covid19PandemicMember2022-03-012023-02-28

0001616262rmcf:WellsFargoBankMemberus-gaap:LineOfCreditMember2022-03-012023-02-28

0001616262rmcf:WellsFargoBankMemberus-gaap:LineOfCreditMember2023-02-28

0001616262rmcf:WellsFargoBankMemberus-gaap:LineOfCreditMemberus-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMember2021-03-012022-02-28

0001616262rmcf:WellsFargoBankMemberus-gaap:LineOfCreditMemberus-gaap:SecuredOvernightFinancingRateSofrOvernightIndexSwapRateMember2023-02-28

0001616262rmcf:EquityIncentivePlan2007Member2022-02-28

0001616262rmcf:EquityIncentivePlan2007Member2022-03-012023-02-28

0001616262rmcf:EquityIncentivePlan2007Member2023-02-28

0001616262us-gaap:RestrictedStockUnitsRSUMember2022-02-28

0001616262us-gaap:RestrictedStockUnitsRSUMember2020-02-29

0001616262us-gaap:RestrictedStockUnitsRSUMember2020-03-012021-02-28

0001616262us-gaap:RestrictedStockUnitsRSUMember2023-02-28

0001616262srt:MaximumMember2022-11-30

0001616262srt:MinimumMember2022-11-30

0001616262rmcf:RetailLeasesMember2022-03-012023-02-28

0001616262rmcf:RetailLeasesMember2021-03-012022-02-28

0001616262rmcf:RetailLeasesMember2020-03-012021-02-28

0001616262us-gaap:AccountingStandardsUpdate201602Member2019-03-01

0001616262rmcf:LeasesForEquipmentMember2023-02-28

0001616262rmcf:WarehouseSpaceMember2023-02-28

0001616262rmcf:WarehouseSpaceMember2022-02-28

0001616262rmcf:WarehouseSpaceMember2021-02-28

00016162622022-03-012022-11-30

0001616262us-gaap:RestrictedStockUnitsRSUMemberrmcf:FormerSeniorVicePresidentSalesAndMarketingMember2022-09-302022-09-30

0001616262rmcf:FormerSeniorVicePresidentSalesAndMarketingMember2022-09-302022-09-30

0001616262rmcf:FormerSeniorVicePresidentSalesAndMarketingMember2022-09-30

utr:M

0001616262srt:MinimumMember2022-03-012022-11-30

0001616262srt:MaximumMember2022-03-012022-11-30

00016162622021-10-02

00016162622021-10-022021-10-02

0001616262rmcf:WarrantToPurchaseCommonStockMembersrt:MaximumMember2019-12-20

0001616262rmcf:WarrantToPurchaseCommonStockMember2019-12-20

0001616262rmcf:WarrantToPurchaseCommonStockMember2019-12-202019-12-20

0001616262rmcf:USwirlSegmentMember2022-02-28

0001616262us-gaap:OperatingSegmentsMemberrmcf:FranchisingMember2022-03-012023-02-28

0001616262us-gaap:OperatingSegmentsMemberrmcf:ManufacturingMember2022-03-012023-02-28

0001616262us-gaap:OperatingSegmentsMemberrmcf:RetailSegmentMember2022-03-012023-02-28

0001616262us-gaap:OperatingSegmentsMemberrmcf:USwirlSegmentMember2022-03-012023-02-28

0001616262us-gaap:OperatingSegmentsMemberus-gaap:AllOtherSegmentsMember2022-03-012023-02-28

0001616262us-gaap:IntersegmentEliminationMemberrmcf:FranchisingMember2022-03-012023-02-28

0001616262us-gaap:IntersegmentEliminationMemberrmcf:ManufacturingMember2022-03-012023-02-28

0001616262us-gaap:IntersegmentEliminationMemberrmcf:RetailSegmentMember2022-03-012023-02-28

0001616262us-gaap:IntersegmentEliminationMemberrmcf:USwirlSegmentMember2022-03-012023-02-28

0001616262us-gaap:IntersegmentEliminationMemberus-gaap:AllOtherSegmentsMember2022-03-012023-02-28

0001616262rmcf:FranchisingMember2022-03-012023-02-28

0001616262rmcf:ManufacturingMember2022-03-012023-02-28

0001616262rmcf:RetailSegmentMember2022-03-012023-02-28

0001616262rmcf:USwirlSegmentMember2022-03-012023-02-28

0001616262us-gaap:AllOtherSegmentsMember2022-03-012023-02-28

0001616262rmcf:FranchisingMember2023-02-28

0001616262rmcf:ManufacturingMember2023-02-28

0001616262rmcf:RetailSegmentMember2023-02-28

0001616262rmcf:USwirlSegmentMember2023-02-28

0001616262us-gaap:AllOtherSegmentsMember2023-02-28

0001616262us-gaap:OperatingSegmentsMemberrmcf:FranchisingMember2021-03-012022-02-28

0001616262us-gaap:OperatingSegmentsMemberrmcf:ManufacturingMember2021-03-012022-02-28

0001616262us-gaap:OperatingSegmentsMemberrmcf:RetailSegmentMember2021-03-012022-02-28

0001616262us-gaap:OperatingSegmentsMemberrmcf:USwirlSegmentMember2021-03-012022-02-28

0001616262us-gaap:OperatingSegmentsMemberus-gaap:AllOtherSegmentsMember2021-03-012022-02-28

0001616262us-gaap:IntersegmentEliminationMemberrmcf:FranchisingMember2021-03-012022-02-28

0001616262us-gaap:IntersegmentEliminationMemberrmcf:ManufacturingMember2021-03-012022-02-28

0001616262us-gaap:IntersegmentEliminationMemberrmcf:RetailSegmentMember2021-03-012022-02-28

0001616262us-gaap:IntersegmentEliminationMemberrmcf:USwirlSegmentMember2021-03-012022-02-28

0001616262us-gaap:IntersegmentEliminationMemberus-gaap:AllOtherSegmentsMember2021-03-012022-02-28

0001616262rmcf:FranchisingMember2021-03-012022-02-28

0001616262rmcf:ManufacturingMember2021-03-012022-02-28

0001616262rmcf:RetailSegmentMember2021-03-012022-02-28

0001616262rmcf:USwirlSegmentMember2021-03-012022-02-28

0001616262us-gaap:AllOtherSegmentsMember2021-03-012022-02-28

0001616262rmcf:FranchisingMember2022-02-28

0001616262rmcf:ManufacturingMember2022-02-28

0001616262rmcf:RetailSegmentMember2022-02-28

0001616262us-gaap:AllOtherSegmentsMember2022-02-28

0001616262us-gaap:OperatingSegmentsMemberrmcf:FranchisingMember2020-03-012021-02-28

0001616262us-gaap:OperatingSegmentsMemberrmcf:ManufacturingMember2020-03-012021-02-28

0001616262us-gaap:OperatingSegmentsMemberrmcf:RetailSegmentMember2020-03-012021-02-28

0001616262us-gaap:OperatingSegmentsMemberrmcf:USwirlSegmentMember2020-03-012021-02-28

0001616262us-gaap:OperatingSegmentsMemberus-gaap:AllOtherSegmentsMember2020-03-012021-02-28

0001616262us-gaap:IntersegmentEliminationMemberrmcf:FranchisingMember2020-03-012021-02-28

0001616262us-gaap:IntersegmentEliminationMemberrmcf:ManufacturingMember2020-03-012021-02-28

0001616262us-gaap:IntersegmentEliminationMemberrmcf:RetailSegmentMember2020-03-012021-02-28

0001616262us-gaap:IntersegmentEliminationMemberrmcf:USwirlSegmentMember2020-03-012021-02-28

0001616262us-gaap:IntersegmentEliminationMemberus-gaap:AllOtherSegmentsMember2020-03-012021-02-28

0001616262rmcf:FranchisingMember2020-03-012021-02-28

0001616262rmcf:ManufacturingMember2020-03-012021-02-28

0001616262rmcf:RetailSegmentMember2020-03-012021-02-28

0001616262rmcf:USwirlSegmentMember2020-03-012021-02-28

0001616262us-gaap:AllOtherSegmentsMember2020-03-012021-02-28

0001616262rmcf:FranchisingMember2021-02-28

0001616262rmcf:ManufacturingMember2021-02-28

0001616262rmcf:RetailSegmentMember2021-02-28

0001616262rmcf:USwirlSegmentMember2021-02-28

0001616262us-gaap:AllOtherSegmentsMember2021-02-28

00016162622022-03-012022-05-31

00016162622022-06-012022-08-31

00016162622022-09-012022-11-30

00016162622022-12-012023-02-28

00016162622021-03-012021-05-31

00016162622021-06-012021-08-31

00016162622021-09-012021-11-30

00016162622021-12-012022-02-28

0001616262rmcf:LossOnDistributionOfAssetsMember2022-03-012023-02-28

0001616262rmcf:LossOnDistributionOfAssetsMember2021-03-012022-02-28

0001616262rmcf:LossOnDistributionOfAssetsMember2020-03-012021-02-28

0001616262rmcf:ContestedSolicitationOfProxiesMember2022-03-012023-02-28

0001616262rmcf:ContestedSolicitationOfProxiesMember2021-03-012022-02-28

0001616262rmcf:ContestedSolicitationOfProxiesMember2020-03-012021-02-28

0001616262us-gaap:RestrictedStockUnitsRSUMemberrmcf:PresidentAndChiefExecutiveOfficerMemberrmcf:LetterAgreementMember2022-03-012023-02-28

0001616262us-gaap:RestrictedStockUnitsRSUMemberrmcf:PresidentAndChiefExecutiveOfficerMemberrmcf:LetterAgreementMember2021-11-032021-11-03

0001616262rmcf:PresidentAndChiefExecutiveOfficerMemberrmcf:LetterAgreementMember2022-03-012023-02-28

0001616262rmcf:PresidentAndChiefExecutiveOfficerMemberrmcf:LetterAgreementMember2021-03-012022-02-28

0001616262us-gaap:RestrictedStockUnitsRSUMemberrmcf:PresidentAndChiefExecutiveOfficerMemberrmcf:LetterAgreementMember2021-03-012022-02-28

0001616262rmcf:USwirlIncMember2022-03-012023-02-28

0001616262rmcf:USwirlIncMember2021-03-012022-02-28

0001616262rmcf:USwirlIncMember2020-03-012021-02-28

0001616262rmcf:USwirlIncMember2023-02-28

0001616262rmcf:USwirlIncMember2022-02-28

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended February 28, 2023

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________ to __________

Commission file number: 001-36865

Rocky Mountain Chocolate Factory, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 47-1535633 |

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

265 Turner Drive

Durango, CO 81303

(Address of principal executive offices, including ZIP code)

(970) 259-0554

(Registrant’s telephone number, including area code)

Securities Registered Pursuant To Section 12(b) Of The Act:

| Title of each class | | Trading

Symbol(s) | | Name of each exchange on which registered |

| Common Stock, $0.001 par value per share | | RMCF | | The Nasdaq Global Market |

Securities Registered Pursuant To Section 12(g) Of The Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ |

| | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the registrant’s common stock (based on the closing price as quoted on the Nasdaq Global Market on August 31, 2022, the last business day of the registrant’s most recently completed second fiscal quarter) held by non-affiliates was $36,755,278. For purposes of this calculation, shares of common stock beneficially owned by each executive officer and director and by holders of more than 10% of the registrant’s outstanding common stock have been excluded since those persons may under certain circumstances be deemed to be affiliates of the registrant. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of May 19, 2023, there were 6,283,450 shares of the registrant’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement in connection with the 2023 Annual Meeting of Stockholders (the “Proxy Statement”) are incorporated by reference in Part III of this Annual Report on Form 10-K. The Proxy Statement will be filed with the Securities and Exchange Commission within 120 days of the registrant’s fiscal year ended February 28, 2023.

ROCKY MOUNTAIN CHOCOLATE FACTORY, INC.

FORM 10-K

TABLE OF CONTENTS

Cautionary Note Regarding Forward-Looking Statements

This Annual Report on Form 10-K (“Annual Report”) contains statements of our expectations, intentions, plans and beliefs that constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and are intended to come within the safe harbor protection provided by those sections. All statements other than statements of historical fact are “forward-looking statements,” including, but not limited to, any projections of earnings, revenue or other financial items; any statements of the plans, strategies and objectives of management, including for future operations, or capital expenditures; any statements concerning proposed new products, services, or developments; any statements regarding future economic conditions or performance; any statements of belief or expectation; and any statements of assumptions underlying any of the foregoing or other future events. Forward-looking statements may include, among others, words such as “will,” “may,” “would,” “could,” “might,” “likely,” “objective,” “predict,” “project,” “drive,” “seek,” “aim,” “target,” “outlook,” “continue” “intend,” “believe,” “expect,” “anticipate,” “should,” “plan,” “estimate,” “potential,” or similar expressions. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those projected, anticipated, or implied. Although it is not possible to predict or identify all such risks and uncertainties, they include, but are not limited to, the factors discussed in Item 1A. “Risk Factors” of Part I of this Annual Report and as described elsewhere in this Annual Report. All forward-looking statements are expressly qualified in their entirety by these and other cautionary statements that we make from time to time in our other SEC filings and public communications. You should evaluate forward-looking statements in the context of these risks and uncertainties and are cautioned not to place undue reliance on such statements. Forward-looking statements in this Annual Report are made only as of the date hereof, and we undertake no obligation to update or revise any forward-looking statement except as may be required by law.

PART I.

ITEM 1. BUSINESS

Our Company

Rocky Mountain Chocolate Factory, Inc., a Delaware corporation, and its subsidiaries (collectively, the “Company,” “Rocky Mountain,” “we,” “us,” or “our”), including its operating subsidiary with the same name, Rocky Mountain Chocolate Factory, Inc., a Colorado corporation (“RMCF”), is an international franchisor, confectionery manufacturer and retail operator. Founded in 1981, we are headquartered in Durango, Colorado and manufacture an extensive line of premium chocolate candies and other confectionery products. Our revenues and profitability are derived principally from our franchised/licensed system of retail stores that feature chocolate and other confectionary products. We also sell our candy in select locations outside of our system of retail stores. As of February 28, 2023, there was one Company-owned, 111 licensee-owned and 157 franchised Rocky Mountain Chocolate Factory stores operating in 37 states, Panama, and the Philippines.

In fiscal year (“FY”) 2023, approximately half (50%) of the products sold at Rocky Mountain Chocolate Factory stores were prepared on premises. We believe that in-store preparation of products creates a special store ambiance, and the aroma and sight of products being made attracts foot traffic and assures customers that products are fresh.

Our principal competitive strengths lie in our brand name recognition, our reputation for the quality, variety and taste of our products, the ambiance of our stores, our expertise in the manufacture of chocolate candy products and the merchandising and marketing of confectionary products, and the control and training infrastructures we have implemented to ensure consistent customer service and execution of successful practices and techniques at our stores.

We believe our manufacturing expertise and reputation for quality has facilitated the sale of select products through specialty markets. We are currently selling our products in a select number of specialty markets, including wholesale, fundraising, corporate sales, mail order, private label and internet sales (collectively “Omni-channel”).

Our consolidated revenues in FY 2023 were primarily derived from three principal sources: (i) sales to franchisees and other third parties of chocolates and other confectionery products manufactured by us (77%-76%-80% in 2023, 2022 and 2021 respectively); (ii) sales at Company-owned stores of chocolates and other confectionery products (including products manufactured by us) (3%-4%-4%), and (iii) the collection of initial franchise, royalties and marketing fees from franchisees (20%-20%-16%). For FY 2023, nearly all of our revenues were derived from domestic sources, with less than 1% derived from international sources. As described below, the Company sold its frozen yogurt business subsequent to the end of FY 2023.

Sale of Frozen Yogurt Business

On May 1, 2023, subsequent to the end of fiscal year 2023, the Company completed the sale of substantially all of the assets of its wholly-owned subsidiary and frozen yogurt business, U-Swirl International, Inc. (“U-Swirl”). The aggregate sale price of U-Swirl was $2.75 million, consisting of (i) $1.75 million in cash and (ii) $1.0 million evidenced by a three-year secured promissory note. The business divestiture of the U-Swirl segment was preceded by a separate sale of the Company’s three owned U-Swirl locations on February 24, 2023. With the sale of our frozen yogurt segment on May 1, 2023, we continue to focus on our confectionery business to further enhance our competitive position and operating margin, simplify our business model, and deliver sustainable value to our stockholders. The consolidated financial statements present the historical financial results of the former U-Swirl segment as discontinued operations for all periods presented. See Note 20 of the Notes to Consolidated Financial Statements included in Item 8, “Financial Statements and Supplementary Data“, of this Annual Report for information on this divestiture.

Business Strategy

Our updated long term strategic objective is to build upon the solid market position of our brand and high-quality products to create a world-class experience for consumers of premium chocolate products, whether in premium confection stores operated by our franchisees or by us, or purchased from us through a variety of other channels. We intend to lead this effort through the delivery of an exceptional store experience and development of category leadership through innovation. To accomplish this objective, we will employ a business strategy that includes the elements set forth below.

Product Quality and Variety

We maintain the gourmet taste and quality of our chocolate candies by using the finest chocolate and other wholesome ingredients. We use our proprietary recipes, primarily developed by our master candy makers. A typical Rocky Mountain Chocolate Factory store offers up to 100 of our chocolate candies throughout the year and as many as 200, including many packaged candies, during the holiday seasons. Individual stores also offer numerous varieties of gourmet caramel apples as well as other products prepared in the store from Company recipes. We have enhanced our product development and innovation capabilities through the Company’s recent hiring of its first ever R&D Director.

Store Atmosphere and Ambiance

We seek to establish a fun, enjoyable and inviting atmosphere in each of our store locations. Unlike most other confectionery stores, each Rocky Mountain Chocolate Factory store prepares numerous products, including caramel apples, in the store. In-store preparation is designed to be both fun and entertaining for customers. We believe the in-store preparation and aroma of our products enhances the ambiance at Rocky Mountain Chocolate Factory stores, is fun and entertaining for our customers and conveys an image of freshness and homemade quality. The Company has been, and is committed to, deploying increased headquarter resources to our store network to further improve the store experience and enhance profitability, all while maintaining brand standards.

Site Selection

Careful selection of a new retail site is critical to the success of our stores. We consider many factors in identifying suitable sites, including tenant mix, visibility, attractiveness, accessibility, level of foot traffic and occupancy costs. Final site selection occurs only after our senior management has approved the site.

Increase Same Store Retail Sales at Existing Rocky Mountain Chocolate Factory Stores

We seek to increase profitability of our store system by increasing sales at existing store locations through a combination of offering the optimal product assortment to stores, improving order fulfillment, facilitating increased product availability to stores through streamlined logistics, and providing Company personnel to help franchised locations improve their sales and profitability. We recognize that a 10% system-wide increase in revenues from our existing store base would be the equivalent of opening 15 new stores.

Changes in system-wide domestic same store retail sales at Rocky Mountain Chocolate Factory locations are as follows:

| FY 2019 compared to FY 2018 |

|

|

1.0 |

% |

| FY 2020 compared to FY 2019 |

|

|

0.5 |

% |

| FY 2021 compared to FY 2020 |

|

|

(24.8 |

)% |

| FY 2022 compared to FY 2021 |

|

|

62.4 |

% |

| FY 2023 compared to FY 2022 |

|

|

0.5 |

% |

Same store sales declined during FY 2021 primarily as a result of nearly all of the franchise stores being directly and negatively impacted by public health measures taken in response to COVID-19, with nearly all locations experiencing reduced operations as a result of, among other things, modified business hours and store and mall closures. This decline was offset by a same store sales increase during FY 2022 when store operations resumed normal operations following the initial impacts of COVID-19.

We are working towards a full rebranding of our offerings, as well as a redesign of our stores, both of which, we believe, will improve the store experience and have a positive impact on same store sales.

Increased System-Wide Annual Unit Volume (“AUV”)

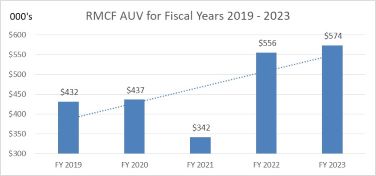

A critical part of success in selling new franchises is the attractiveness of store level economics, which include robust and expanding system-wide annual sales. For FY 2023 our AUV was approximately $574,000, which represents a 31% increase from the FY 2020 AUV of $437,000. We look to build upon this momentum and our goal is to achieve system-wide AUV of $800,000 by fiscal year 2028.

Enhanced Operating Efficiencies

We have added highly experienced manufacturing and supply chain talent in order to bring sustained operating efficiencies to the factory. In addition to such actions and investing in new and more efficient factory equipment, we are rationalizing our portfolio of products and streamlining production lines to both reduce labor needs as well as improve product quality and consistency. We seek to achieve $1.2MM in annual operating cost improvements at our current level of production by the middle of fiscal year 2025, and achieve a 30% factory gross margin by fiscal year 2028.

Expansion Strategy

We are continually exploring opportunities to grow our brand and expand our business. Key elements of our expansion strategy are set forth below.

Unit Growth

We continue to pursue unit growth opportunities in locations where we have traditionally been successful, by improving and expanding our retail store concepts and product portfolio, and by targeting high pedestrian traffic environments.

High Traffic Environments

We currently establish franchised stores in the following environments: regional centers, outlet centers, tourist areas, street fronts, airports, other entertainment-oriented environments and festival and community centers. We have established business relationships with most of the major developers in the United States and believe that these relationships provide us with the opportunity to take advantage of attractive sites in new and existing real estate environments.

Multi-unit Operators

We have traditionally focused our franchise marketing efforts largely on single unit operators. By further enhancing our brand strength, product offering, and strong store experience, coupled with enhanced economics, we seek going forward to appeal more, and market to, multi-unit operators looking to expand their portfolio of franchised opportunities into a premium chocolate franchise concept.

Expanded Omni-channel Selling Efforts

We have acquired new sales and marketing talent, as well as developed new third party relationships, to facilitate the sale and distribution of Rocky Mountain Chocolate Factory products to channels outside of the franchisee network.

Rocky Mountain Chocolate Factory Name Recognition and New Market Penetration

We believe the visibility of our stores and the high foot traffic at many of our locations has generated strong name recognition of Rocky Mountain Chocolate Factory and demand for our franchises. The Rocky Mountain Chocolate Factory system currently is concentrated in the western and Rocky Mountain region of the United States, but growth has generated a gradual easterly momentum as new stores have been opened in the eastern half of the country. We believe this growth has further increased our name recognition and demand for our franchises. We believe that distribution of Rocky Mountain Chocolate Factory products through our Omni-channel business also increases name recognition and brand awareness in areas of the country in which we have not previously had a significant presence and we believe it will also improve and benefit our entire store system.

We seek to establish a fun, enjoyable and inviting atmosphere in each of our store locations. Unlike many other confectionery stores, each Rocky Mountain Chocolate Factory store prepares numerous products, including caramel apples, in the store. In FY 2023, an average of approximately half of the revenues of franchised stores were generated by sales of products prepared on premises. In-store preparation is designed to be both fun and entertaining for customers and we believe the in-store preparation and aroma of our products enhance the ambiance at Rocky Mountain Chocolate Factory stores, is fun and entertaining for our customers and conveys an image of freshness and homemade quality.

The average store size is approximately 1,000 square feet, approximately 650 square feet of which is selling space. Most stores are open seven days a week.

In January 2007, we began testing co-branded locations, such as the co-branded stores with Cold Stone Creamery. Co-branding a location is a vehicle to exploit retail environments that would not typically support a stand-alone Rocky Mountain Chocolate Factory store. Co-branding can also be used to more efficiently manage rent structure, payroll and other operating costs in environments that have not historically supported stand-alone Rocky Mountain Chocolate Factory stores. As of February 28, 2023, Cold Stone Creamery franchisees operated 101 co-branded locations, our U-Swirl franchisees operated 10 co-branded locations.

International units in operation were as follows on February 28, 2023:

| Rocky Mountain Chocolate Factory |

|

|

|

|

| The Republic of Panama |

|

|

1 |

|

| The Republic of the Philippines |

|

|

3 |

|

| Total |

|

|

4 |

|

Products and Packaging

We produce approximately 400 chocolate candies and other confectionery products using proprietary recipes developed primarily by our master candy makers. These products include many varieties of clusters, caramels, creams, toffees, mints and truffles. These products are offered for sale and also configured into approximately 250 varieties of packaged assortments. During the Christmas, Easter and Valentine's Day holiday seasons, we may make as many as 90 items, including many candies offered in packages, that are specially designed for such holidays. A typical Rocky Mountain Chocolate Factory store offers up to 100 of these approximately 400 chocolate candies and other confectionery products throughout the year and up to an additional 90 during the holiday seasons. Individual stores also offer more than 15 varieties of caramel apples and other products prepared in the store. In FY 2023, approximately 49% of the revenues of Rocky Mountain Chocolate Factory stores are generated by products manufactured at our factory, 48% by products made in individual stores using our recipes and ingredients purchased from us or approved suppliers and the remaining 3% by products such as ice cream, coffee and other sundries purchased from approved suppliers.

In FY 2023, approximately 15% of our factory sales resulted from the sale of products outside of our system of franchised and licensed locations, which we refer to as Omni-channel customers, compared with 17% of our factory sales resulting from Omni-channel customers in FY 2022. See Item 1A “Risk Factors—Risks Related to Our Company and Strategy—Our Sales to Omni-channel Customers, Customers Outside Our System of Franchised Stores, Are Concentrated Among a Small Number of Customers.” These products are produced using the same quality ingredients and manufacturing processes as the products sold in our network of retail stores.

We use the finest chocolates, nutmeats and other wholesome ingredients in our candies and continually strive to offer new confectionery items in order to maintain the excitement and appeal of our products. We develop special packaging for the Christmas, Valentine's Day and Easter holidays, and customers can have their purchases packaged in decorative boxes and fancy tins throughout the year.

Chocolate candies that we manufacture are sold at prices ranging from $21.95 to $33.30 per pound, with an average price of $26.96 per pound. Franchisees set their own retail prices, though we do recommend prices for all of our products.

Operating Environment

Rocky Mountain Chocolate Factory

We currently establish Rocky Mountain Chocolate Factory stores in six primary environments: outlet centers, festival and community centers, regional centers, tourist areas, street fronts, airports and other entertainment-oriented shopping centers. Each of these environments has a number of attractive features, including high levels of foot traffic. Rocky Mountain Chocolate Factory domestic franchise locations in operation as of February 28, 2023, include:

| Outlet Centers |

|

|

20.9 |

% |

| Festival/Community Centers |

|

|

20.3 |

% |

| Regional Centers |

|

|

18.9 |

% |

| Tourist Areas |

|

|

17.6 |

% |

| Street Fronts |

|

|

10.5 |

% |

| Airports |

|

|

5.9 |

% |

| Other |

|

|

5.9 |

% |

Outlet Centers

As of February 28, 2023, there were approximately 32 Rocky Mountain Chocolate Factory stores in outlet centers. We have established business relationships with a number of the major outlet center developers in the United States. Although not all factory outlet centers provide desirable locations for our stores, we believe our relationships with these developers will provide us with the opportunity to take advantage of attractive sites in new and existing outlet centers.

Festival and Community Centers

As of February 28, 2023, there were approximately 31 Rocky Mountain Chocolate Factory stores in festival and community centers. Festival and community centers offer retail shopping outside of traditional regional and outlet center shopping.

Regional Centers

As of February 28, 2023, there were Rocky Mountain Chocolate Factory stores in approximately 29 regional centers, including a location in the Mall of America in Bloomington, Minnesota. Although they often provide favorable levels of foot traffic, regional centers typically involve more expensive rent structures and competing food and beverage concepts.

Tourist Areas, Street Fronts, Airports and Other Entertainment-Oriented Shopping Centers

As of February 28, 2023, there were approximately 27 Rocky Mountain Chocolate Factory stores in locations considered to be tourist areas. Tourist areas are very attractive locations because they offer high levels of foot traffic and favorable customer spending characteristics, and greatly increase our visibility and name recognition. We believe there are a number of other environments that have the characteristics necessary for the successful operation of Rocky Mountain Chocolate Factory stores such as airports and casinos. As of February 28, 2023, there were 9 franchised Rocky Mountain Chocolate Factory stores at airport locations.

Franchising Program

General

We continue to attract qualified and experienced franchisees, whom we consider to be a vital part of the Company’s continued growth. We believe our relationship with our franchisees is fundamental to the performance of our brand and we strive to maintain a collaborative relationship with our franchisees. Our franchising philosophy is one of service and commitment to our franchise system and we continuously seek to improve our franchise support services. Our concept has been rated as an outstanding franchise opportunity by publications and organizations rating such opportunities. The Rocky Mountain Chocolate Factory concept has frequently been ranked in the Top 500 Franchises by Entrepreneur Magazine. As of February 28, 2023, there were 157 franchised stores in the Rocky Mountain Chocolate Factory system.

Franchisee Sourcing and Selection

The majority of new franchises are awarded to persons referred to us by existing franchisees, to interested consumers who have visited one of our domestic franchise locations and to existing franchisees. We also advertise for new franchisees in national and regional newspapers and online as suitable potential store locations come to our attention. We are exploring the use of third party franchise lead generators to supplement our efforts. Franchisees are currently approved by a committee of the senior executive team based on the applicant's net worth and liquidity, business acumen and prior experience with franchising and/or fast moving consumer goods (“FMCG”), together with an assessment of work ethic and personality compatibility with our operating philosophy.

International Franchising and Licensing

International growth is generally achieved through entry into a Master License Agreement covering specific countries, with a licensee that meets minimum qualifications to develop Rocky Mountain Chocolate Factory in that country. License agreements are generally entered into for a period of 3-10 years and allow the licensee exclusive development rights in a country. Generally, we require an initial license fee and commitment to a development schedule. Active international license agreements in place include the following:

| |

● |

In October 2014, we entered into a Licensing Agreement in the Republic of the Philippines. As of February 28, 2023, three units were operating under the agreement. |

| |

● |

In May 2017, we entered into a Licensing Agreement in the Republic of Panama. As of February 28, 2023, one unit was operating under the agreement. |

Co-Branding

In August 2009, we entered into a Master License Agreement with Kahala Franchise Corp. Under the terms of the agreement, select current and future Cold Stone Creamery franchise stores are co-branded with both the Rocky Mountain Chocolate Factory and the Cold Stone Creamery brands. Locations developed or modified under the agreement are subject to the approval of both parties. Locations developed or modified under the agreement will remain franchisees of Cold Stone Creamery and will be licensed to offer the Rocky Mountain Chocolate Factory brand. As of February 28, 2023, Cold Stone Creamery franchisees operated 101 stores under this agreement.

Additionally, we allow U-Swirl brands to offer Rocky Mountain Chocolate Factory products under terms similar to other co-branding agreements. As of February 28, 2023, there were 10 U-Swirl cafés offering Rocky Mountain Chocolate Factory products.

Training and Support

Each domestic franchisee owner/operator and each store manager for a domestic franchisee is required to complete a comprehensive training program in store operations and management. We have established a training center at our Durango headquarters in the form of a full-sized replica of a properly configured and merchandised Rocky Mountain Chocolate Factory store. Topics covered in the training course include our philosophy of store operation and management, customer service, merchandising, pricing, cooking, inventory and cost control, quality standards, record keeping, labor scheduling and personnel management. Training is based on standard operating policies and procedures contained in an operations manual provided to all franchisees, which the franchisee is required to follow by terms of the franchise agreement. Additionally, and importantly, trainees are provided with a complete orientation to our operations by working in key factory operational areas and by meeting with members of our senior management.

Our operating objectives include providing knowledge and expertise in merchandising, marketing and customer service to all front-line store level employees to maximize their skills and ensure that they are fully versed in our proven techniques.

We provide ongoing support to franchisees through our field consultants, who maintain regular and frequent communication with the stores by phone and by site visits. The field consultants also review and discuss store operating results with the franchisee and provide advice and guidance in improving store profitability and in developing and executing store marketing and merchandising programs.

Quality Standards and Control

The franchise agreements for Rocky Mountain Chocolate Factory brand franchisees require compliance with our procedures of operation and food quality specifications and permit audits and inspections by us.

Operating standards for Rocky Mountain Chocolate Factory brand stores are set forth in operating manuals. These manuals cover general operations, factory ordering, merchandising, advertising and accounting procedures. Through their regular visits to franchised stores, our field consultants audit performance and adherence to our standards. We have the right to terminate any franchise agreement for non‑compliance with our operating standards. Products sold at the stores and ingredients used in the preparation of products approved for on-site preparation must be purchased from us or from approved suppliers.

The Franchise Agreement: Terms and Conditions

The domestic offer and sales of our franchise concepts are made pursuant to the respective franchise disclosure document prepared in accordance with federal and state laws and regulations. States that regulate the sale and operation of franchises require a franchisor to register or file certain notices with the state authorities prior to offering and selling franchises in those states.

Under the current form of our domestic franchise agreements, franchisees pay us (i) an initial franchise fee for each store, (ii) royalties based on monthly gross sales, and (iii) a marketing fee based on monthly gross sales. Franchisees are generally granted exclusive territory with respect to the operation of their stores only in the immediate vicinity of their stores. Chocolate products not made on premises by franchisees must be purchased from us or approved suppliers. The franchise agreements require franchisees to comply with our procedures of operation and food quality specifications, to permit inspections and audits by us and to remodel stores to conform with standards then in effect. We may terminate the franchise agreement upon the failure of the franchisee to comply with the conditions of the agreement and upon the occurrence of certain events, such as insolvency or bankruptcy of the franchisee or the commission by the franchisee of any unlawful or deceptive practice, which in our judgment is likely to adversely affect the system. Our ability to terminate franchise agreements pursuant to such provisions is subject to applicable bankruptcy and state laws and regulations. See “Regulation” below for additional information.

The agreements prohibit the transfer or assignment of any interest in a franchise without our prior written consent. The agreements also give us a right of first refusal to purchase any interest in a franchise if a proposed transfer would result in a change of control of that franchise. The refusal right, if exercised, would allow us to purchase the interest proposed to be transferred under the same terms and conditions and for the same price as offered by the proposed transferee.

The term of each franchise agreement is ten years, and franchisees have the right to renew for one additional ten-year term.

Franchise Financing

We do not typically provide prospective franchisees with financing for their stores for new or existing franchises, but we have developed relationships with several sources of franchisee financing to whom we will refer franchisees. Typically, franchisees have obtained their own sources of such financing and have not required our assistance. In the normal course of business, we extend credit to customers, primarily franchisees that satisfy pre-defined credit criteria, for inventory and other operational costs.

In select instances, we have provided limited financing to franchisees. As a result, as of February 28, 2023, we have approximately $200,000 of notes receivable as a result of financing our franchisees. When we finance franchisees the notes are secured by the assets financed.

Company Store Operations

As of February 28, 2023, there was one Company-owned Rocky Mountain Chocolate Factory store. Our flagship store, located in Durango, Colorado, (“Flagship Store”) provides a training ground for Company personnel and a controllable testing ground for new products and promotions, operating and training methods and merchandising techniques, which may then be incorporated into the franchise store operations.

Manufacturing Operations

General

We manufacture our chocolate candies at our manufacturing facility in Durango, Colorado. All products are produced consistent with our philosophy of using the finest high-quality ingredients to achieve our marketing motto of “The Peak of Perfection in Handmade Chocolates®.”

We have always believed that we should control the manufacturing of our own chocolate products. By controlling manufacturing, we can better maintain our high product quality standards, offer unique proprietary products, manage costs, control production and shipment schedules and potentially pursue new or under-utilized distribution channels.

Manufacturing Processes

The manufacturing process primarily involves cooking or preparing candy centers, including nuts, caramel, peanut butter, creams and jellies, and then coating them with chocolate or other toppings. All of these processes are conducted in carefully controlled temperature ranges, and we employ strict quality control procedures at every stage of the manufacturing process. We use a combination of manual and automated processes at our factory. Although we believe that it is currently preferable to perform certain manufacturing processes, such as the dipping of some large pieces by hand, automation increases the speed and efficiency of the manufacturing process. We have from time to time automated certain processes formerly performed by hand where it has become cost-effective for us to do so without compromising product quality or appearance.

We also seek to ensure the freshness of products sold in Rocky Mountain Chocolate Factory stores with frequent shipments. Most Rocky Mountain Chocolate Factory stores do not have significant space for the storage of inventory, and we encourage franchisees and store managers to order only the quantities that they can reasonably expect to sell within approximately two to four weeks. For these reasons, we generally do not have a significant backlog of orders.

The manufacture and sale of consumer food products is highly regulated. In the U.S., our activities are subject to regulation by various government agencies, including the Food and Drug Administration (“FDA”), the Department of Agriculture, the Federal Trade Commission, the Department of Commerce and the Environmental Protection Agency, as well as various state and local agencies. Similar agencies also regulate our businesses outside of the U.S.

The Company has a product quality and safety program. This program is integral to our supply chain platform and is intended to ensure that all products we purchase, manufacture and distribute are safe, are of high quality and comply with applicable laws and regulations. Through our product quality and safety program, we evaluate our supply chain including ingredients, packaging, processes, products, distribution and the environment to determine where product quality and safety controls are necessary. We follow the FDA mandated Hazard Analysis and Risk-based Preventive Controls which includes a 12 step process to determine risks based on individual processes. To support this hazard analysis model, and in accordance with private and federal mandated requirements, we also adhere to all good manufacturing practices ("GMPs") including several supporting policies and procedures that ensure all risks identified are in control. Various government agencies and third-party firms, as well as our quality assurance staff, conduct audits of all facilities that manufacture our products to ensure effectiveness and compliance with our program and applicable laws and regulations.

Ingredients

The principal ingredients used in our products are chocolate, nuts, sugar, corn syrup, cream and butter. The factory receives shipments of ingredients daily. To ensure the consistency of our products, we buy ingredients from a limited number of reliable suppliers. In order to ensure a continuous supply of chocolate and certain nuts, we frequently enter into purchase contracts of between six to eighteen months for these products. Because prices for these products may fluctuate, we may benefit if prices rise during the terms of these contracts, but we may be required to pay above-market prices if prices fall. We have one or more alternative sources for most essential ingredients and therefore believe that the loss of any one supplier would not have a material adverse effect on our business or results of operations. We currently purchase small amounts of finished candy from third parties on a private label basis for sale in Rocky Mountain Chocolate Factory stores. As a result of recent macro-economic inflationary trends and disruptions to the global supply chain, we have experienced and may continue to experience higher raw material, labor, and freight costs.

Trucking Operations

We operate eight trucks and ship a substantial portion of our products from the factory on our own fleet. Our trucking operations enable us to deliver our products to the stores quickly and cost-effectively. In addition, we back-haul our own ingredients and supplies, as well as products from third parties, on return trips, which helps achieve even greater efficiencies and cost savings.

Marketing

General

We rely primarily on in-store promotion and point-of-purchase materials to promote the sale of our products. The monthly marketing fees collected from franchisees are used by us to develop new packaging and in-store promotion and point-of-purchase materials, and to create and update our local store marketing guides and materials.

We focus on local store marketing efforts by providing customizable marketing materials, including advertisements, coupons, flyers and brochures generated by our in-house Creative Services department. The department works directly with franchisees to implement local store marketing programs.

We have not historically, and do not intend to, engage in national traditional media advertising in the near future. Consistent with our commitment to community support, we seek opportunities to participate in local and regional events, sponsorships and charitable causes. This support leverages low-cost, high return publicity opportunities for mutual gain partnerships.

Internet and Social Media

We’ve initiated a robust program to leverage the marketing benefits of various social media outlets. These lower-cost marketing opportunities leverage the positive feedback of our customers, expanding brand awareness through a customer’s network of contacts. Complementary to local store marketing efforts, these networks also provide a medium for us to communicate regularly and authentically with customers. When possible, we work to facilitate direct relationships between our franchisees and their customers. We use social media as a tool to build brand recognition, increase repeat exposure, and enhance dialogue with consumers about their preferences and needs. The majority of stores have location-specific Facebook® and Instagram® accounts dedicated to helping customers interact directly with their local store. Proceeds from the monthly marketing fees collected from franchisees are used by us to facilitate and assist stores in managing their online presence consistent with our brand and marketing efforts.

Competition

The retailing of confectionery products is highly competitive. We and our franchisees compete with numerous businesses that offer products similar to those offered by our stores. Many of these competitors have greater name recognition and financial, marketing and other resources than us. In addition, there is intense competition among retailers for attractive commercial real estate sites suitable for Rocky Mountain Chocolate Factory stores, store personnel and qualified franchisees.

We believe that our principal competitive strengths lie in our name recognition and our reputation for the quality, value, variety and taste of our products and the ambiance of our stores; our knowledge and experience in applying criteria for the selection of new store locations; our expertise in merchandising and marketing of chocolate and other candy products; and the control and training infrastructures we have implemented to ensure execution of successful practices and techniques at our store locations. In addition, by controlling the manufacturing of our own chocolate products, we can better maintain our high product quality standards for those products, offer proprietary products, manage costs, control production and shipment schedules and pursue new or under-utilized distribution channels.

Trade Name and Trademarks

The trade name “Rocky Mountain Chocolate Factory®,” the phrases, “The Peak of Perfection in Handmade Chocolates®“, “America's Chocolatier®“ as well as all other trademarks, service marks, symbols, slogans, emblems, logos and designs used in the Rocky Mountain Chocolate Factory system, are our proprietary rights. We believe all of the foregoing are of material importance to our business. The trademark “Rocky Mountain Chocolate Factory” is registered in the United States and Canada. Applications to register the Rocky Mountain Chocolate Factory trademark have been filed and/or obtained in certain foreign countries.

We have not attempted to obtain patent protection for the proprietary recipes developed by our master candy-maker and instead rely upon our ability to maintain the confidentiality of those recipes.

Environmental Matters

We are not aware of any federal, state, local or international environmental laws or regulations that we expect to materially affect our earnings or competitive position or result in material capital expenditures. However, we cannot predict the effect of possible future environmental legislation or regulations on our operations. During FY 2023, we had no material environmental compliance-related capital expenditures, and no such material expenditures are anticipated in FY 2024.

Seasonal Factors

Our sales and earnings are seasonal, with significantly higher sales and earnings occurring during key holidays, such as Christmas, Easter and Valentine's Day, and the U.S. summer vacation season than at other times of the year, which may cause fluctuations in our quarterly results of operations. In addition, quarterly results have been, and in the future are likely to be, affected by the timing of new store openings, the sale of franchises and the timing of purchases by customers outside our network of franchised locations. Because of the seasonality of our business, results for any quarter are not necessarily indicative of the results that may be achieved in other quarters or for a full fiscal year.

Regulation

Company-owned and franchised Rocky Mountain Chocolate Factory stores are subject to licensing and regulation by the health, sanitation, safety, building and fire agencies in the state or municipality where located. Difficulties or failures in obtaining the required licensing or approvals could delay or prevent the opening of new stores. New stores must also comply with landlord and developer criteria.

Many states have laws regulating franchise operations, including registration and disclosure requirements in the offer and sale of franchises. We are also subject to the Federal Trade Commission regulations relating to disclosure requirements in the sale of franchises and ongoing disclosure obligations.

Additionally, certain states have enacted and others may enact laws and regulations governing the termination or non-renewal of franchises and other aspects of the franchise relationship that are intended to protect franchisees, including among other things, limitation on the duration and scope of non-competition provisions applicable to franchisees. Although these laws and regulations, and related court decisions, may limit our ability to terminate franchises and alter franchise agreements, we do not believe that such laws or decisions will have a material adverse effect on our franchise operations. However, the laws applicable to franchise operations and relationships continue to develop, and we are unable to predict the effect on our intended operations of additional requirements or restrictions that may be enacted or of court decisions that may be adverse to franchisors.

Federal and state environmental regulations have not had a material impact on our operations but more stringent and varied requirements of local governmental bodies with respect to zoning, land use and environmental factors could delay the construction of new stores, increase our capital expenditures and thereby decrease our earnings and negatively impact our competitive position.

Companies engaged in the manufacturing, packaging and distribution of food products are subject to extensive regulation by various governmental agencies. A finding of failure to comply with one or more regulations could result in the imposition of sanctions, including the closing of all or a portion of our facilities for an indeterminate period of time. Our product labeling is subject to and complies with the Nutrition Labeling and Education Act of 1990 and the Food Allergen Labeling and Consumer Protection Act of 2004.

We provide a limited amount of trucking services to third parties, to fill available space on our trucks. Our trucking operations are subject to various federal and state regulations, including regulations of the Federal Highway Administration and other federal and state agencies applicable to motor carriers, safety requirements of the Department of Transportation relating to interstate transportation and federal, state and Canadian provincial regulations governing matters such as vehicle weight and dimensions.